/NVIDIA%20Corp%20logo%20on%20phone-by%20Evolf%20via%20Shutterstock.jpg)

Tensions between Israel and Iran had been building, with the United States stepping into the equation and keeping global markets uneasy. The risk of disruption to oil supplies and trade routes had investors on edge. But sentiment shifted after President Donald Trump signaled a pause in military action, hinting that diplomacy might take over, at least for now.

That shift quickly found its way into tech stocks, including NVIDIA Corporation (NVDA). The company isn’t just another chipmaker – it’s the backbone of the artificial intelligence (AI) revolution, powering everything from data centers to advanced computing systems. NVDA’s rally has been powerful, though not without pauses. After flirting with a rare $5 trillion valuation, the stock saw some pullback as concerns around high valuations and heavy AI infrastructure spending kicked in.

With geopolitical fears cooling off, investors rushed back into high-growth names tied to AI demand, pushing NVDA stock higher. But here’s the catch. Despite long-term AI tailwinds, NVDA trades at premium levels. While short-term sentiment has turned positive, with NVDA snapping its four-day losing streak, should investors jump in now or stay patient for a more comfortable entry point?

About NVIDIA Stock

Santa Clara-based Nvidia hardly needs an introduction. Once celebrated as the king of gaming graphics, it quietly reinvented itself as the backbone of modern computing. Its GPUs now power data centers, AI, robotics, and immersive digital worlds. The CUDA software platform locked developers into a powerful ecosystem, turning Nvidia into an industry standard rather than a supplier. With a market capitalization of nearly $4.27 trillion, Jensen Huang’s company has become the engine of the AI economy.

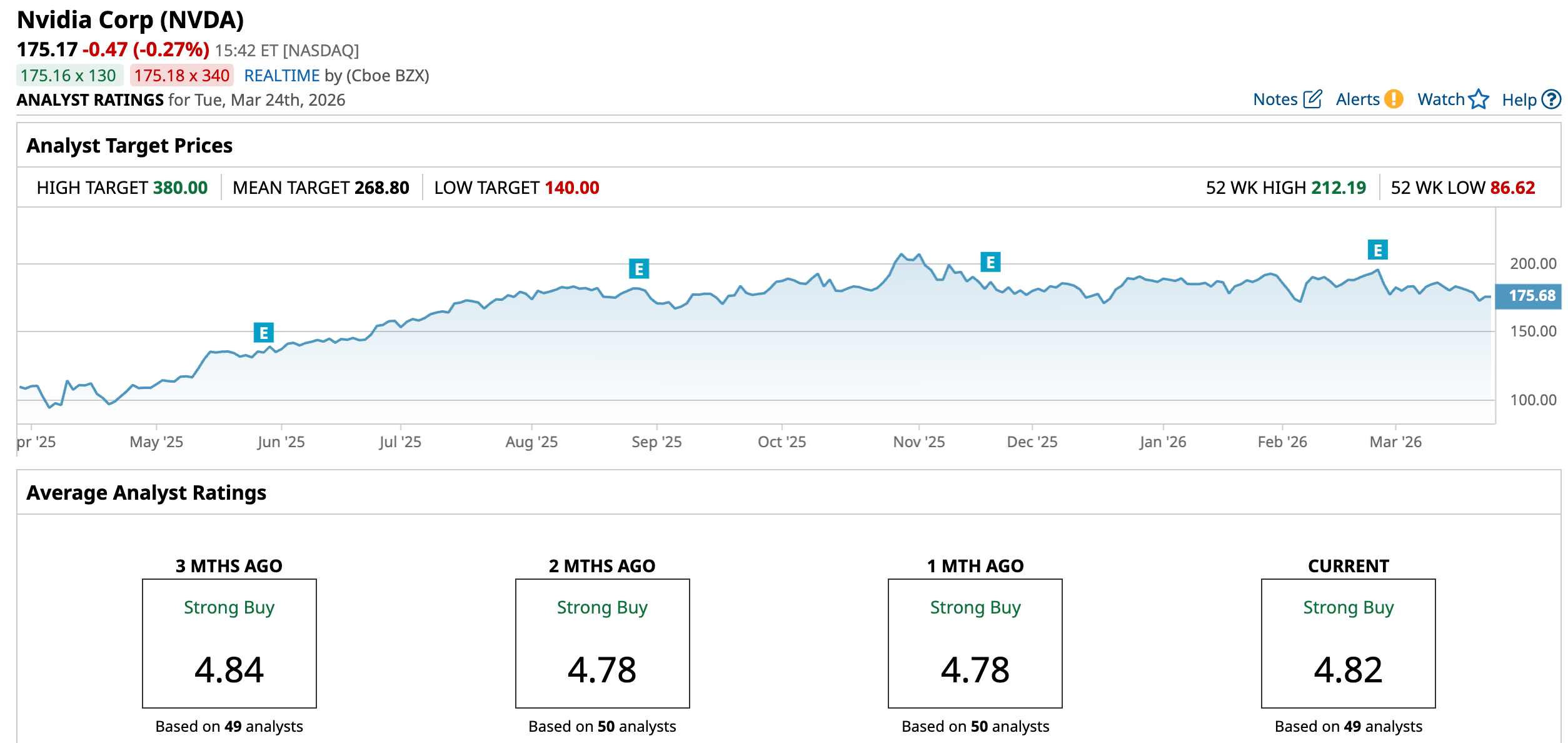

Over the past year, NVDA stock’s journey has felt less like a straight sprint and more like a calculated climb. The stock surged in strong bursts, then paused, almost as if the market was catching its breath before the next move. After touching a high of $212.19 in late October, it pulled back nearly 17%, reminding investors that even leaders need cooling-off phases. Yet zooming out, the bigger picture still looks solid, with the stock up 44.36% over the past 52 weeks.

Technically, momentum has softened, but it has not cracked. The 14-day Relative Strength Index, once overheated above 80, has cooled to 41.60 and is now gradually trending upward, hinting that selling pressure is easing. It’s a phase of reset, not retreat, where the stock quietly builds strength for its next potential move.

Meanwhile, trading volumes are showing more red bars, hinting at some selling pressure in the near term. The MACD oscillator adds a cautious tone, with the MACD line slipping below the signal line and the histogram turning slightly negative. Nevertheless, the move is not aggressive or accelerating. It feels more like a cooldown phase than a real shift in trend.

When we look at NVIDIA today, the valuation might seem a bit stretched at first glance, especially compared to other AI tech players. The stock is priced at around 22.55 times forward adjusted earnings and 11.55 times forward sales. But this is not a typical semiconductor stock. NVIDIA sits at the center of the AI wave, where growth is faster, and margins are stronger. So, the premium starts to feel more like a reflection of leadership than excess. In fact, even after its massive rally over the past few years, its current valuation sits below its own past highs.

What adds stability is NVIDIA’s disciplined approach. It has quietly paid dividends for over a decade, showing it’s not just a growth story, but a maturing, cash-generating powerhouse as well.

NVIDIA Beats Q4 Numbers

On Feb. 25, NVIDIA reported its fiscal fourth-quarter 2026 results, and the numbers rose past expectations, reinforcing why the AI chip giant continues to dominate this space. Revenue surged to $68.1 billion, marking a sharp 73.2% year-over-year (YOY), while adjusted earnings climbed 82% annually to $1.62 per share.

The real engine behind this growth was its data center business. As tech giants and enterprises race to build AI infrastructure, demand for Nvidia’s chips has been relentless. Data center revenue alone hit $62.3 billion, up roughly 75% YOY. Even gaming, once its core identity, showed strong momentum, rising 47% annually to $3.7 billion as newer architectures gained traction.

What stands out is the company’s financial strength. NVIDIA exited the year with $62.6 billion in cash, cash equivalents, and marketable securities as of Jan. 25, 2026, with relatively low debt, building a balance sheet that gives it flexibility and confidence. It generated $34.9 billion in free cash flow in just one quarter, helping push its full-year total close to $96.6 billion.

That strength is flowing back to shareholders, too. During fiscal 2026, NVIDIA returned $41.1 billion through buybacks and dividends, while still keeping $58.5 billion repurchase authorization available. At the same time, it’s not slowing down on innovation. New AI chips like Vera Rubin promise massive efficiency gains, with even more advanced systems already in the pipeline.

Looking ahead, the tone remains upbeat. With CEO Jensen Huang calling demand “skyrocketing,” Nvidia expects revenue around $78 billion in the fiscal first-quarter 2027, suggesting this AI-driven growth story is far from over.

Meanwhile, analysts tracking NVIDIA estimate Q1 fiscal year 2027 EPS to grow 118.2% YOY to $1.68. For the full fiscal year 2027, the bottom line is expected to surge 67.6% annually to $7.66 per share, followed by another 30.9% YOY increase in fiscal 2028 to $10.03 per share.

What Do Analysts Expect for Nvidia Stock?

After wrapping up its latest GTC event, NVIDIA left analysts with one big idea to chew on – a future where data center revenue could cross $1 trillion by 2027. That headline number grabbed attention, but Melius Research analyst Ben Reitzes believes the real story runs even deeper.

He points out that this $1 trillion projection includes only certain chip systems, such as Blackwell and Rubin, leaving out several newer growth drivers discussed at the event. When adjusted for that, the opportunity looks even bigger. Even after trimming the estimate to about $835 billion for the next two years, it still sits above Street expectations, suggesting meaningful upside. In fact, Reitzes sees potential for over $100 billion in additional revenue, which could lift EPS by roughly $1.00 in fiscal 2027 and about $1.50 per share in fiscal 2028, assuming strong margin flow-through.

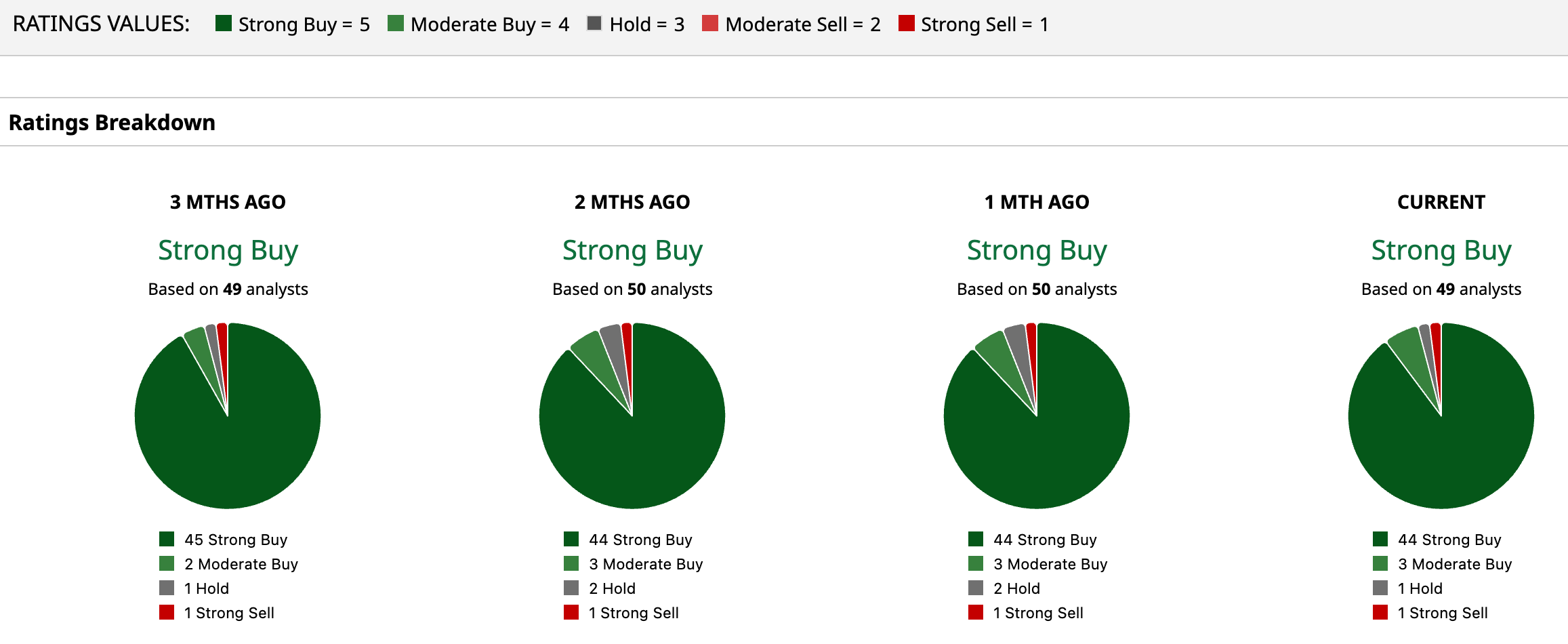

Beyond the numbers, NVIDIA’s growing strength in AI inference, new platforms, and its expanding end-to-end ecosystem position it as more than just a chipmaker – it is becoming the backbone of AI infrastructure. With this momentum, Reitzes maintains a “Buy” rating and a Street-high $380 price target, signaling confidence that Nvidia’s growth story is far from fully priced in.

Overall, analysts are upbeat about NVDA’s growth potential, giving the stock a consensus rating of “Strong Buy.” Of the 49 analysts covering the stock, 44 advise a “Strong Buy,” while three suggest “Moderate Buy,” one advises a “Hold,” and only one suggests a “Strong Sell.”

The average analyst price target for NVDA is $268.80, indicating potential upside of 53.5%. Ben Reitzes Street-high target price of $380 suggests that the stock could rally as much as 116.9% from here.

Final Thoughts on NVIDIA

Donald Trump's signaling of a pause in the war, and the rebound in tech stocks and NVDA recently, reflect how quickly sentiment can shift when macro fears ease. The temporary cooling in Middle East conflict concerns has helped steady expectations around energy markets and global growth, factors that tech stocks are especially sensitive to.

NVIDIA’s core story – AI leadership, strong execution, and expanding partnerships across industries – continues to play out steadily. Still, not everything is one-way traffic. Rich valuations and growing capital commitments add a layer of caution. NVIDIA’s long-term path looks solid, but near-term moves may stay uneven. For those already in, it remains a hold grounded in fundamentals. And for those watching from the sidelines, patience could be just as important as confidence right now.